OVER 25 YEARS… BUILDING. DEVELOPING. HONING. PROVING OUR LOSS ASSESSMENT RESOURCES

PLC prides itself on our extensive and expansive “Resource”, representing the country’s leading and foremost experts in their respective fields, as our (and your) “Loss Assessment Team”, strategically positioned Nationwide.

We have spent “Over 25 Years”… Building …Developing…Honing…and… Proving our (and your) “Loss Assessment Resource”, and are confident that same is unmatched in the Market Place. In many instances through the strength and leverage of PLC, and our years of commitment to this “Resource”, we have repositioned the Insurance Company National Resources, (at large), to work in our (your) interest. Hence positioning us (and you) for a Strategic Advantage, positioning the field in our (your) favor, if you will … rather than just leveling the field.

We have developed this unmatched “Resource” to best serve our Clients, as well as our respective Client Groups. We have been able to entrench ourselves with the “Best of the Best”, due to the associated national demand to continually produce and document accurate detail reporting, on “Loss Assessments”, for all facets of Covered Property, under your respective “First Party Property Insurance Contract”, i.e. Insurance Policy.

In addition, to detail and accuracy, same must be achieve timely, in order to expedite filings, so as our firm can quickly file Claim(s), on your behalf, hence expedite PAYMENTS and/or CLAIM SETTLMENTS.

The “Loss Assessment” portion of our services, under contract, is the Foundation, i.e. Brick or Mortar if you will of our firms ability to consistently MAXIMIZE our Clients RECOVERIES, this of, ( See Loss Consulting ).

Our expert’s utilize their vast years of industry experience in their respective “Specialized Fields”, to prepare highly detailed “Loss Assessments”, to not only document “Loss”, i.e. Scope of Damage, but also just as important, if not more important “Value”, i.e. Cost to Repair/Replace or Restore Damaged Property (To Pre Loss Condition). In addition to compiling these reports, our experts are also are instrumental, in the forward support and collaboration of “Claim Presentation”, supporting PLC through affective “Claim Negotiations”, under the respective terms and conditions of the policy, all in support of “MAXIMIZING RECOVERY”, on behalf of our clients, with respects to “Claims Filed”:

The “Loss Assessments” referenced above, are the most common. However, they are not “All Inclusive”, as there are varying “Types” of other “PROPERTY”, requiring “Loss Assessments” which must be expertly develop, to support and document both “Loss” and “Value”, under varying Policies and Coverage Forms, as well be presented in the form and content of a respective “Claim Filing”, and then expertly “Negotiated”, under the Terms and Conditions of the “Insurance Contract”.

The “Loss Assessment”, and the subsequent “Claim Presentation”, i.e. “Claim Filings”, as a result, are considered our firms “Foundation”, to support our “CORE SERVICE”, which is to MAXIMIZE, while also EXPEDITE, “CLAIM RECOVERIES”.

Presentation and accuracy of same are key to our firm’s ability to ensure that our adjusters possess the right “TOOLS”, to affectively present and negotiate claims going forward, so as we can consistently deliver on our “CORE SERVICE”.

We should also note, that it is the “Insured’s Responsibility” under their respective Insurance Policy, to “Document” and/or “Support” their own LOSS and VALUE. Further that the insurance company and their respective Claim Adjusters, Claim Staff and Experts, may do so, but certainly do so on their own behalf, in their own respective interests, and same may or may not be all inclusive, or valued necessarily in the “Insured’s/ Owner’s” best interest, with respects to both Loss and Value.

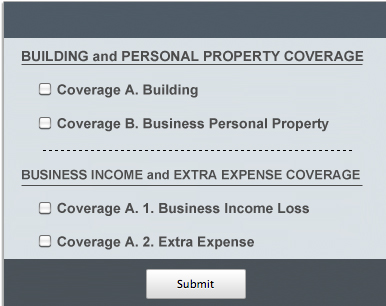

BUILDING LOSS ASSESMENT

Room by Room”, or “Area Defined”, Detail or Description of Damage, coding same in a clear uniform depiction and/or listing of specific Building Loss or Damage, “Item by Item”, representing the “Scope of Damage”. The above correlating with detailed specific Measurement of the Area of Damage, representing “Loss Quantity”, within the same reporting. This reporting also inclusive of “Up To Date”, accurate “Loss Valuation”, (in the form of “Pricing”, inclusive of “Unit Cost Pricing” i.e. “Repair Cost Valuation”, which combines: Labor, Material and Equipment, to Replace Damage Building Property). The above, also inclusive of Costs associated with Demolition and Debris Removal, also inclusive of “Soft Costs”, (Sales Tax, Shipping, Freight, Contractor Overhead and Profit, etc.), and is specific by State and Region.

In summary the above reporting represents our “Building Damage Appraisal”, which encompasses the “Building Loss”. This reporting is combined with various other Supporting Documentation, inclusive of but not limited to: Photographs, Drawings, Diagrams, Inspection Reporting, etc. Same represents our “Building Claim”, to be filed under Coverage A. Building and then professionally negotiated by PLC, our respective staff and affiliates, ensuring our Client’s “Maximum Insurance Recovery”.

*** REPLACEMENT COST (RCV) LESS DEPRECIATION = ACTUAL CASH VALUE (ACV)

*** Our Loss Assessment Experts will calculate and assist our Loss Consultants in Negotiation of Depreciation Amounts, so as to increase ACV Settlements.

*** In addition our Loss Consultants will also assist you in preparation and filing of RCV Claims, for withheld Depreciation (if Coverage is applicable under Your respective Policy).

*** Co-Insurance (Value, Subject to Co-Insurance Percentage must be Equal or Greater than Coverage Limit), or “Loss Payment” will be subject to Co-Insurance Penalty, (If Limits are Lower than Value, Less Co-Insurance Percent), better Defined as Underinsurance. Our Loss Assessment Experts, will assist our Loss Consultants in Valuing Property, so as to confirm accurate Valuations, and support our Loss Consultants in Negotiating Valuations.

UNDERSTANDING THE PROCESS:

WHY A CONTRACTOR’S ESTIMATE IS NOT ENOUGH

Initially it starts with our expert’s initial inspection of risk, which produces a scope of damage and/or scope of repair. In addition to the scope, our experts also complete interior and exterior Diagrams/ Blueprints of the building depicting accurate measurements of floors, walls, ceilings and roofs. Finally our experts then complete a photo analysis depicting the specific damages addressed in the scope of repair as documentation to support allowance. These details are then drafted in appraisal form utilizing state of the art computer software systems. The final product will include a room by room, detailed itemized scope and value of repair inclusive all cost for your state and local, including but not limited to Debris Removal, Permit Fees, Architectural Fees, State Tax and Overhead & Profit calculations.

The idea that you will provide a local contractors estimate to your insurance company as documentation to support repair cost rather than engaging a professional public adjuster and their experts to prepare and document your claim on your behalf, consistently does not work to your advantage and will more than likely result in additional delays and reduction of your maximum insurance recovery.

Most contractors are not insurance restoration experts. They may not be knowledgeable as to how to restore specific damage related to water, heat, smoke and others. In addition they may not be aware of “Hidden” damages that need to be treated or restored utilizing special, specific methods of restoration. Their proposals will lack the detail and documentation necessary to substantiate your loss to your insurance company.

They will also prepare their proposals on the basis of competitiveness in effort to win over the job rather than the maximum amount recoverable for the repair. They will not be able to assist you with other facets of your building loss such as calculations of: Depreciation, Co-Insurance, Broad Evidence, Etc. or assist you with your other loss exposures Personal Property, Additional Living Expense, Business Income Loss, Extra Expense, Etc.

BUSINESS PERSONAL PROPERTY LOSS ASSESSMENT

“Room by Room”, or “Area Defined” Descriptive List of Damage Item(s), inclusive but not limited to: Furniture, Fixtures and Equipment, inclusive of Stock (Finished /Unfinished). Coding same in a clear uniform depiction or listing, i.e. “Damaged Inventory”. The “Items” are reviewed and inspected, as well as their Packaging, in efforts to determine the “Level of Damage”. The items will be evaluated to determine if they can be Restored (To Pre-Loss Condition/Value). If the items cannot be Restored to “Pre-Loss Condition/Value they will be included for REPLACEMENT VALUE, i.e. COST to REPLACE with Items of LIKE, KIND and Quality. In addition Items that cannot be Restored (To Pre-Loss Condition/Value), will be considered for Salvage Value, or alternatively deemed Total Loss (Having No Value).

The “Damaged Items” to be included will represent the “Damaged Inventory”, same are then coded with specific Measurement, which details the “Quantity” of Items Damaged or Lost.

The “Damaged Inventory” in then “PRICED” or “VALUED”, utilizing the “Original Incurred Cost”, and documented utilizing “Historical Invoicing”, and in some instances various Forensic Accounting methods to further document the “VALUE”. Same again is usually based on the “Original Incurred Cost” of the Property, however, in some instances (were coverage exists), it may be included and valued at “Retail Cost”. In this instance we must also include and document respective “Markup Valuations”. The valuation, in addition to “Cost Pricing”, as well as Costs associated with Cartage and Debris Removal (Total Loss Items), also includes, but is not limited to: Sales Tax, Freight, Shipping Costs, Handling Costs, or Other “Soft Costs”, necessary to restore same to PRE-LOSS CONDITION or alternatively REPLACE same with property of Like, Kind and Quality.

In summary the above reporting represents our “Business Personal Property Damage Appraisal”, which encompass the “Damaged Inventory”. This reporting is combined with various other Supporting Documentation, inclusive of, but not limited to: Photographs, Appraisals, Dealer Inspections and Reporting, Value Documentation, Manufacturer Specifications, etc., and represents our “Business Personal Property Claim”, to be filed under Coverage B. Business Personal Property and then professionally negotiated by PLC, our respective staff and affiliates, ensuring our Client’s “Maximum Insurance Recovery”.

*** REPLACEMENT COST (RCV) LESS DEPRECIATION = ACTUAL CASH VALUE (ACV)

*** Our Loss Assessment Experts will calculate and assist our Loss Consultants in Negotiation of Depreciation Amounts, so as to increase ACV Settlements.

*** In addition our Loss Consultants will also assist you in preparation and filing of RCV Claims, for withheld Depreciation (if Coverage is applicable under Your respective Policy).

*** Co-Insurance (Value, Subject to Co-Insurance Percentage must be Equal or Greater than Coverage Limit), or “Loss Payment” will be subject to Co-Insurance Penalty, (If Limits are Lower than Value, Less Co-Insurance Percent), better Defined as Underinsurance. Our Loss Assessment Experts, will assist our Loss Consultants in Valuing Property, so as to confirm accurate Valuations, and support our Loss Consultants in Negotiating Valuations.

BUSINESS INCOME LOSS ASSESMENT

Detailed Analysis of “NET INCOME”, Recoverable Amounts, based specifically on “PROJECTIONS” through various analytics of the respective business financials, inclusive of respective “Historic Sales” to support Positive and/or Negative “SALES TRENDING”. In an efforts to calculate the “PROJECTED NET INCOME AMOUNTS”, which WOULD have been EARNED, had NO LOSS occurred.

*** THE ABOVE OF COURSE TO BE ADJUSTED BY ANY “NET INCOME LOSS AMOUNTS”, IF APPLICABLE.

*** THE ABOVE OF COURSE TO BE ADJUSTED BY ANY “INCOME EARNED” THROUGH THE “PERIOD OF RESTORATION” FROM PARTIAL OPERATIONS.

***TIME ELEMENT SUBJECT TO “PERIOD OF INDEMNITY”, TIME IT TAKES TO REPAIR AND/OR RESTORATE BUILDING AND RESUME BUSINESS OPERATIONS.

In addition we must also perform a Detailed Analysis of any “CONTINUAL NORMAL EXPENSES”, and complete Detailed Reporting on same, as “PROJECTED EXPENSES” to be incurred, to position same for “RECOVERY”. Same is completed through various analytics of the respective business financials, inclusive of respective “Historic Expenses” to support the “PROJECTED CONTINUAL NORMAL EXPENSES”, as well as include Adjustments for the “NON CONTINUAL” and/or “SAVED EXPENSES”, accordingly. The above inclusive of “Payroll”, (if Coverage is applicable).

***TIME ELEMENT SUBJECT TO “PERIOD OF INDEMNITY”, TIME IT TAKES TO REPAIR AND/OR RESTORATE BUILDING AND RESUME BUSINESS OPERATIONS.

The above subject to:

*** Co-Insurance (Value, Subject to Co-Insurance Percentage must be Equal or Greater than Coverage Limit), or “Loss Payment” will be subject to Co-Insurance Penalty, (If Limits are Lower than Value, Less Co-Insurance Percent), better Defined as Under insurance. Our Loss Assessment Experts, will assist our Loss Consultants in Valuing Business income, so as to confirm accurate Valuations, and support our Loss Consultants in Negotiating Valuations.

*** MONTHLY LIMIT OF INDEMNITY (RESTRICTED MONTHLY LIMIT OF INDEMNITY, LIMITED BY FRACTIONAL MONTHLY AMOUNT)

*** MAXIMUM PERIOD OF INDEMNITY (RESTRICTED PERIOD OF INDEMNITY, LIMITED BY DAYS/MONTHS)

EXTENDED PERIOD OF INDEMNITY (EPOI) – LOST INCOME POST RESTORATION, i.e. “Time Element (Loss Coverage) while you RAMP UP OPERATIONS”, either until you Resume Operation to Normal Levels (Had No Loss Occurred), OR Coverage Period is Exhausted, (Standard 30 Days to Restore Income, included in most policies), post the “Period of Restoration”, (Can be Underwritten to include additional “Time Element Coverage Period”). EXTRA EXPENSE Analysis, if Coverage is applicable, is for necessary expenses you incur during the “Period of Restoration” that you would not have incurred, to cover Extra Expenses (other than the expense to repair or replace property) to:

1. Avoid or minimize the “suspension” of business and to continue operations at the described premises or at replacement premises or tempo rary locations, including relocation expenses and costs to equip and operate the replacement location or temporary location.

2. Minimize the “suspension” of business if you cannot continue “operations”, coverage will also extend to repair or replace property, but only to the extent it reduces the amount of loss that would have been payable under Business Income Coverage.